Land Inventory Never Came Back

As Kevin Warsh told the Senate in his recent hearing that the Federal Reserve must stay in its lane and focus on price stability, available land price data was released with implications for the housing shortage.

The headlines have spent the last 18 months focused on the supply wave of 2023 and 2024—the largest delivery of new apartments since the 1980s. Yes, we are currently working through that inventory, and yes, it has created temporary rent pressure as operators lean on concessions to find occupancy.

But there is a less-discussed side effect of that historic boom: it effectively consumed much low-hanging fruit of developable land.

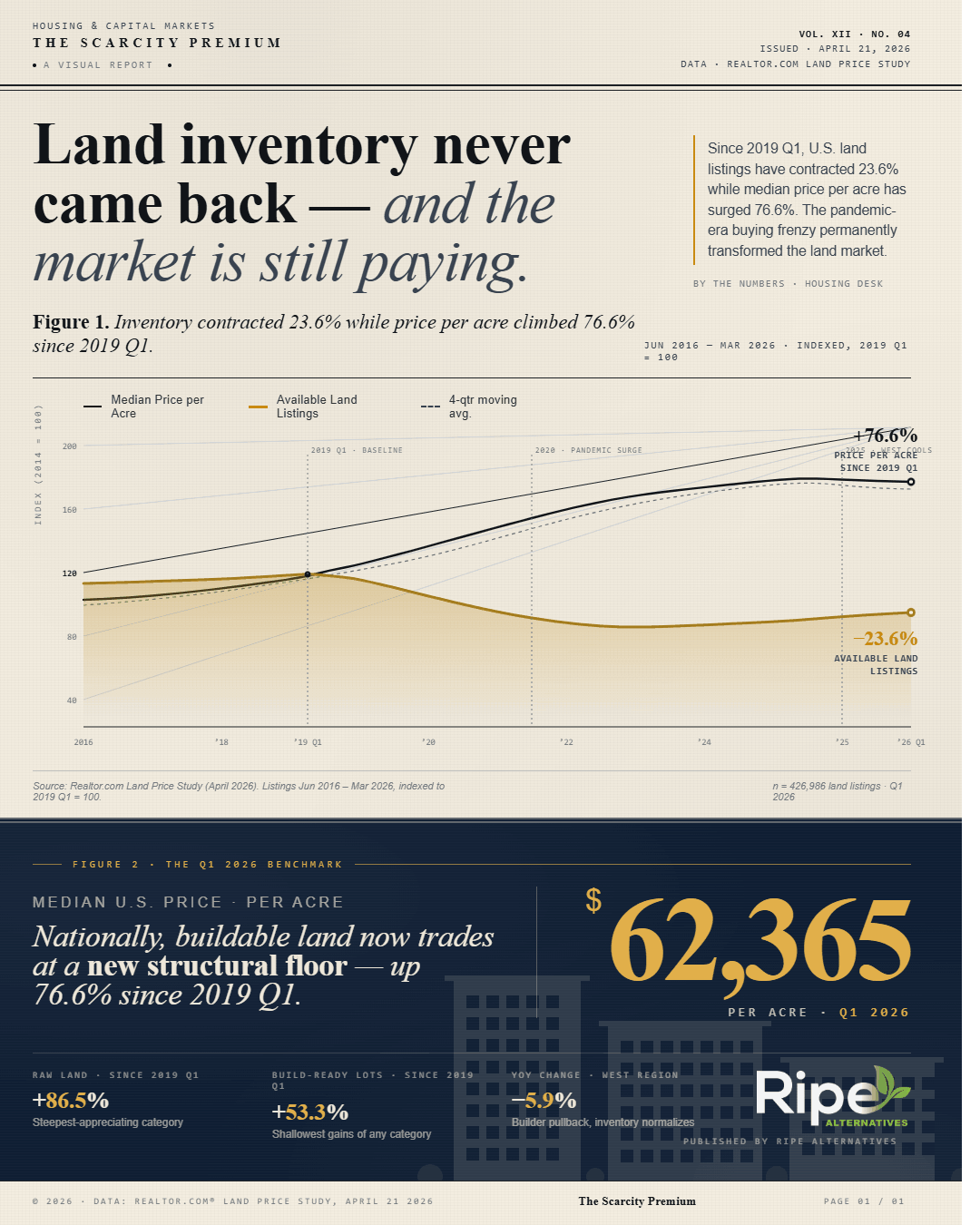

According to the new April 2026 Realtor.com Land Price Study, land inventory is still down nearly 24% from pre-pandemic levels. While national land prices have softened by a marginal 0.5% this year, they remain 76% higher than in 2019.

Here is why this matters for the defensive Class B apartment investor: The land-grab of the last few years, combined with persistently high labor costs, has set a new floor for replacement costs. It is no longer just expensive to build, it is structurally difficult because the most viable parcels in some locations are already gone.

The Rent vs. Buy Savings Gap: A concurrent report also confirms that renting remains the only logical choice for many. Renters in the top 50 metros are currently saving an average of $920 per month compared to the cost of buying a starter home. In markets like Seattle and LA, that renting discount exceeds $2,000.

Persistent Class B Demand: As the 2023-24 supply wave (which was 85% luxury Class A) is absorbed, the lack of new workforce housing starts becomes glaring. We are entering a period where the gap between Class B rents and Class A concession rents will close, but the supply of the former remains fixed.

If the Warsh Era at the Fed brings a smaller balance sheet and a focus on fundamental value, real estate success will be less about riding a cheap-debt wave and more about owning assets that are impossible to replicate at today's prices.

We aren't chasing the next big boom. We’re holding the line on existing, high-demand supply that the market can no longer afford to build.